Nemo.money on AI-Guided Investing & Regulation

By Bits of Us — August 20, 2025

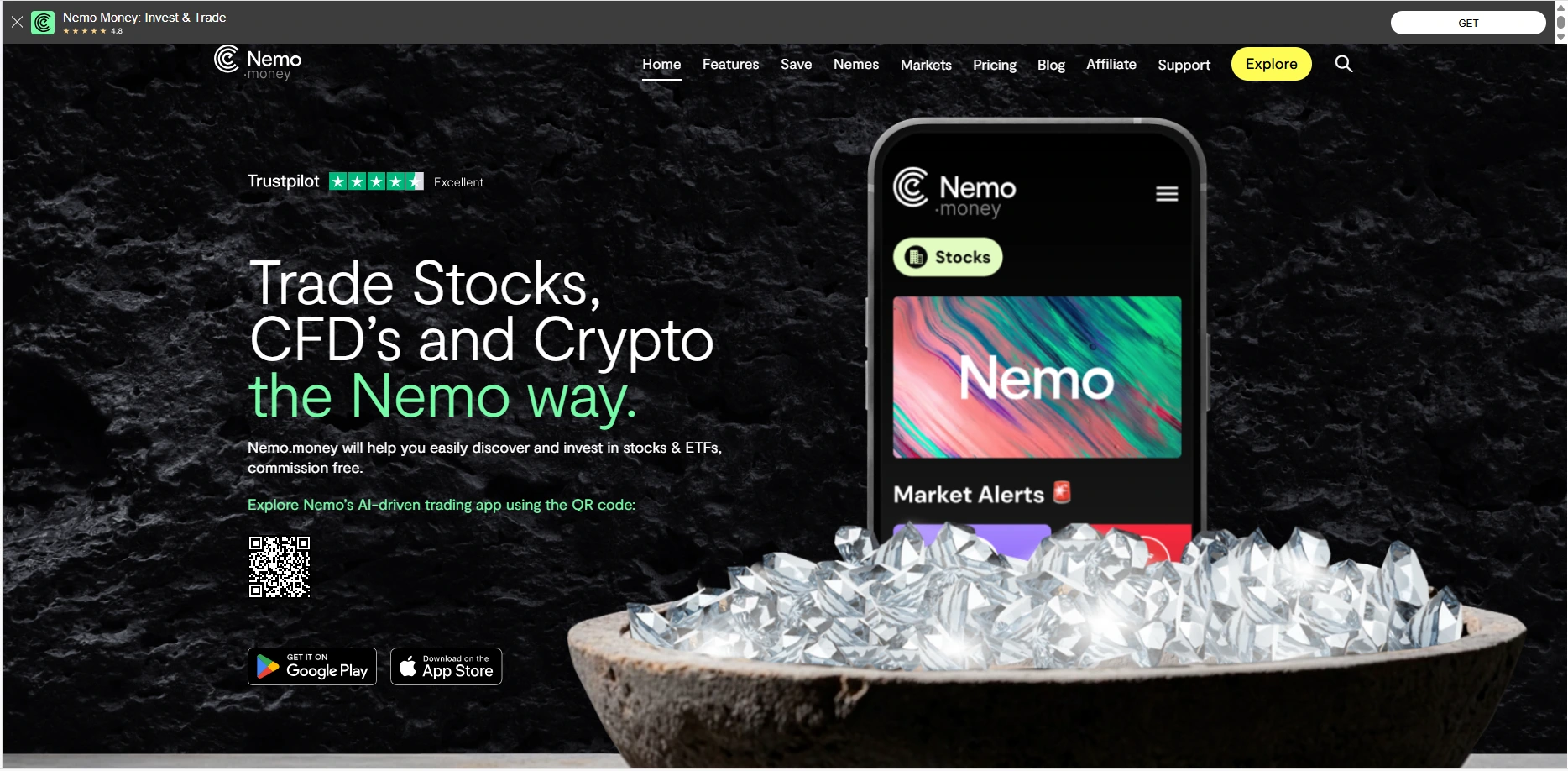

Short summary: Nemo.money — the retail-investing app built by Exinity and regulated in the Abu Dhabi Global Market (ADGM) — is positioning itself as a mass-market, AI-first investing experience. Its recent product moves and public comments from CEO Nicholas Scott show a two-track strategy: use AI to empower novices with personalized, explainable portfolio insights while designing privacy and compliance guardrails that fit the UAE/ADGM regulatory environment. This article unpacks how Nemo’s AI features work in practice, the benefits and pitfalls of AI-guided retail investing, the regulatory landscape shaping those features, and what responsible product design should look like going forward. nemo.moneyCryptoSlate

1. Why Nemo.money matters right now

Nemo.money is not the first app to promise “AI investing”, but its timing and regulatory posture matter. The app combines commission-free multi-asset trading (stocks, ETFs, CFDs, crypto) with an embedded AI assistant and thematic discovery tools (“nemes”) aimed at simplifying investment discovery for retail users. Nemo presents itself as a learning-first product — an investing app and a teacher in one — and it’s backed by a legacy financial group (Exinity) and regulated by ADGM’s Financial Services Regulatory Authority. That combination — AI convenience + a recognized regulatory home — is why Nemo’s ongoing product announcements and public commentary are worth watching for investors, policy makers, and fintech competitors. nemo.moneyCryptoSlate

Two recent, concrete signals illustrate Nemo’s direction. First, product releases this year included “AI Personalized Portfolio Insights,” a feature that applies machine learning to suggest portfolio adjustments, identify diversification gaps, and surface thematic opportunities. Second, the company’s CEO Nicholas Scott recently discussed the product’s approach to data veracity, user privacy, and how regulatory choice (ADGM vs. UK oversight) affects feature design — tellingly, Nemo explicitly frames the UAE regulatory environment as comparatively progressive for fintech innovation. Those announcements are both practical (new features for users) and strategic (shaping investor trust). EIN PresswireCryptoSlate

2. What Nemo’s AI actually does (product anatomy)

When a company claims “AI-guided investing,” the phrase can mean anything from simple rule-based alerts to live, adaptive portfolio optimizers. Nemo’s publicly-documented stack and product marketing suggest several distinct capabilities:

-

Personalized Portfolio Insights: automated analysis that flags portfolio concentration, asset correlations, and risk exposures. The system suggests “what if” adjustments and how those changes would have affected historical risk/return. Nemo marketed a launch of such a feature earlier this year. EIN Presswire

-

Thematic Discovery (“Nemes”): curated groups of stocks tied to macro or sector trends (e.g., “AI chips”, “clean energy”), surfaced by a combination of editorial curation and algorithmic signals. The aim is to turn research into one-tap allocations for beginners. nemo.money

-

Natural-Language Q&A / Education: an in-app “Nemo AI” that answers beginner questions, explains investing terms, and offers bite-sized lessons — effectively a tutoring layer to increase financial literacy. Nemo’s learning hub and blog posts highlight this function. nemo.money

-

Signal fusion across public data: parsing market data, news, social trends, and analyst consensus to identify opportunities. Play-store descriptions and marketing materials imply the app blends multiple data sources into its signals. Google Play

-

Privacy-forward analytics and segregation of funds: while not an AI feature per se, Nemo highlights data protection, SSL encryption, and fund segregation (with SIPC protection for eligible accounts) — a trust play for users concerned about handing over sensitive financial profiles to an AI. nemo.money

Taken together, these features position Nemo as a hybrid between a robo-advisor and a retail trading app: more directive than pure order-execution apps, but less prescriptive (and more “education-first”) than fully automated wealth managers.

3. The user value proposition — who benefits and how

AI-guided investing can deliver clear, measurable benefits at three levels:

-

Beginner investors: the largest cohort Nemo targets. AI can reduce friction by translating complex analytics into plain-language suggestions, showing the consequences of portfolio changes, and offering curated thematic buckets that align with users’ interests (e.g., “AI stocks” or “clean energy”).

-

Time-constrained retail traders: people who want opportunity discovery without hours of research. AI does the heavy lifting: scanning thousands of tickers, aggregating signals, and surfacing candidates with one tap.

-

Financial-literate users seeking augmentation: investors who don’t want a black-box robo but appreciate insight augmentation — e.g., AI that runs scenario analysis or highlights correlation risk they might have missed.

Nemo’s product choices — emphasis on explanation, educational content, and opt-in discovery groups — read as an attempt to maximize those benefits while minimizing overreach. The learning hub and “Nemo AI” Q&A feature underscore a product-first approach that favors guided autonomy: the app nudges rather than replaces decision-making. nemo.money

4. The real risks of AI in retail investing

There are real and well-documented risks whenever algorithmic guidance touches financial decision-making. Companies like Nemo must face three categories of concern:

A. Model risk and overfitting

AI models trained on historical patterns or social signals can produce plausible-sounding recommendations that fail in live markets. Backtests can be overstated; correlations that look stable will break during market stress. If Nemo’s suggestions rely on models not stress-tested across regimes, users could misinterpret historical fit for predictive power.

B. Explainability and behavioral bias

Even when a model provides a correct signal, the way it presents information matters. Simplified recommendations can trigger overconfidence, herding, or “set-and-forget” behavior. Good UI/UX must present uncertainty clearly (probabilities, scenario bands) and warn against binary interpretation of nuanced signals.

C. Data quality & adversarial signals

AI systems ingest broad data: news, filings, social sentiment. That opens exposure to misinformation, pump-and-dump manipulations, and low-quality sources that can bias the signal. Nemo’s emphasis on “truthful data” in public comments is exactly aimed at this problem — but engineering solutions (source vetting, provenance tracking, anomaly detection) must be baked into pipelines. CryptoSlate

Regulation, discussed next, shapes how these risks are managed in product design.

5. Regulation as a product constraint — ADGM and cross-jurisdictional reality

Nemo operates under Abu Dhabi Global Market (ADGM) FSRA regulation and markets globally. ADGM has been active in fintech and digital-asset policy experimentation, and Nemo leans on that regulatory badge as a trust signal. Being ADGM-regulated means Nemo must meet specific requirements around custody, AML/KYC, and data protection — but it doesn’t automatically harmonize the app with other regulators (e.g., FCA in the UK, SEC in the US). Nemo’s public messaging contrasts “progressive” UAE regulation with slower UK oversight — a positioning that reveals both opportunity and friction. nemo.moneyCryptoSlate

Key regulatory implications for AI-driven investing apps like Nemo:

-

Disclosure & suitability: regulators typically require that investment recommendations be suitable for a user’s profile. If an AI suggests asset allocations, the app must demonstrate how it assesses suitability (risk tolerance, investment horizon, knowledge). This is non-trivial when recommendations are generated dynamically.

-

Explainability & consumer protection: some regulators are moving toward explicit rules about explainability in algorithmic advice. Nemo’s educational layer helps, but regulators could mandate standardized disclosures about model inputs, limitations, and historical performance ranges.

-

Data governance & privacy: ADGM has explicit data protection rules; operating across markets, Nemo must manage cross-border data flows and user consent. Transparent logging of what data the AI uses and how it’s stored will be essential.

-

Market integrity & manipulation safeguards: if thematic discovery drives flows into thinly-traded instruments, exchanges and regulators may scrutinize whether algorithmic signals are amplifying volatility or enabling manipulative behaviors.

For Nemo, being ADGM-regulated is a pragmatic choice that enables product rollout in a supportive jurisdiction. But scaling into major markets will require alignment with local regulators’ expectations for AI-driven financial advice. Nemo’s CEO has publicly acknowledged these trade-offs in interviews and podcasts, which signals awareness but not necessarily full compliance roadmaps. CryptoSlateMEXC

6. How Nemo’s approach maps to responsible AI principles

Responsible AI in finance is not an abstract ideal — it’s a practical checklist. Below I map Nemo’s public features and statements to core responsible-AI principles and call out what’s visible and what needs more evidence.

Principle: Safety & Robustness

-

Visible: Nemo advertises portfolio stress tests and scenario analysis.

-

Gap: Public descriptions don’t disclose model validation, adversarial testing, or out-of-sample robustness metrics. Nemo should publish at least summary statistics about model performance across regimes.

Principle: Explainability & Transparency

-

Visible: The product emphasizes user-facing explanations and educational content. CEO commentary stresses “truthful data.”

-

Gap: There’s no public, standardized disclosure that shows how recommendations are generated, inputs used, or error bands. A short “model card” for major features would help.

Principle: Fairness & Non-discrimination

-

Visible: Nemo’s focus is on universal access and financial literacy.

-

Gap: No public audits or third-party fairness assessments are reported. The app should ensure model behavior doesn’t systematically disadvantage particular demographics (e.g., language, region, socioeconomic status).

Principle: Privacy & Data Governance

-

Visible: Nemo highlights ADGM data-protection compliance and encryption, and it segregates user funds per SIPC protections where applicable.

-

Gap: How long behavioral data are retained, whether data are used to train cross-user models, and opt-out pathways for model training are not detailed publicly.

Principle: Accountability & Redress

-

Visible: As a regulated firm, Nemo has regulatory touchpoints and customer support channels.

-

Gap: Formal procedures for when AI-generated advice causes documented harm — e.g., dispute resolution, compensation mechanisms, human-review escalation — should be publicly explained.

Meeting these gaps would not only reduce regulatory risk but increase user trust — and trust is a fungible competitive advantage in fintech.

7. Practical design patterns Nemo (and others) should follow

Below are practical product and governance design patterns that would make Nemo’s AI guidance safer and more useful:

-

Model Cards & Feature Fact Sheets: Publish concise, nontechnical summaries about each AI feature: inputs, outputs, performance metrics, training data sources, limitations, and last update timestamp.

-

Explainable Recommendations: Show counterfactuals — “If you reduced position X by 10%, your portfolio volatility would change by Y%” — instead of only binary “buy/sell” nudges. Include confidence intervals and scenario outcomes.

-

Human-in-the-loop for High-impact Actions: For higher-risk moves (large leveraged positions, high concentration changes), require manual confirmation and offer human advisor review or a cooling-off period.

-

Consent & Opt-out Controls: Let users opt out of having their data used for model retraining; provide clear options for sharing or not sharing behavioral data.

-

Audit Trails & Explainability Logs: Keep auditable logs of recommendations and the data the model used when producing them. These logs help in disputes and regulatory inquiries.

-

Stress-testing & Regime Simulation: Regularly run models in historical stress periods (2008, 2020, 2022 drawdowns) and publish anonymized summaries.

-

Third-party Audits & Bug Bounties: Invite independent model audits and hold bounty programs for adversarial input discovery.

-

Align Incentives with User Outcomes: Avoid gamified features or engagement hooks that push users to trade more; align monetization so that long-term portfolio health is rewarded.

If Nemo adopts these patterns and documents them publicly, it would set a strong example for responsible AI in retail investing.

8. The role of regulation — enabling safe innovation vs. imposing brake

Regulation is a blunt tool when poorly targeted, but done right it creates predictable guardrails that enable innovation. ADGM’s fintech-friendly posture has made it an attractive jurisdiction for firms that want to test new products with clear rules. Nemo leverages that environment to push AI-driven features to market more quickly than might be possible in more conservative jurisdictions.

However, as Nemo scales, the company will face three regulatory realities:

-

Local suitability rules: Many jurisdictions require explicit suitability assessments before recommendations. Nemo will need modularized suitability logic to meet each market’s test.

-

Cross-border data rules: Privacy laws like GDPR or equivalent regimes require strict data transfer and consent mechanisms. Nemo must separate product behavior by region when necessary.

-

Algorithmic oversight expectations: Regulators are increasingly focused on algorithmic systems that materially affect consumers. Expect rules on model documentation, consumer disclosures, and possibly notification requirements for high-impact algorithmic decisions.

Regulators should aim to be clear about desired outcomes (consumer protection, market integrity, non-discrimination) rather than prescribing exact engineering approaches, but they will demand transparency and evidence. Nemo’s public emphasis on explainability and truthful data is a good start — but regulatory compliance will require operational manuals, audits, and governance processes that go beyond marketing language. CryptoSlate+1

9. Where Nemo can lead the market — and where it can learn

Nemo’s strengths that could become market-leading:

-

User-first educational framing: packaging AI advice as education and scenario analysis reduces the “AI told me to do it” failure mode.

-

Thematic, discoverable investing: for novice users, well-curated themes lower the barrier to participation and improve engagement.

-

A strong regulatory anchor (ADGM): this facilitates credibility and may accelerate partnerships with banks or stablecoin rails for settlement.

Areas where Nemo should learn from other leaders:

-

Transparency discipline from healthcare ML: publish nontechnical model summaries and safety testing reports.

-

Robustness practices from trading shops: stress-testing and worst-case scenario planning that trading firms use for algorithmic strategies.

-

Client outcomes focus from wealth managers: move beyond short-term engagement metrics to measures of client financial outcomes over 1–5 year horizons.

If Nemo stitches those lessons into its product roadmap, it could build a “safe growth” playbook that balances mass adoption with consumer protection.

10. Scenario: A responsible rollout for a new AI-driven feature

Imagine Nemo wants to ship a new “auto-rebalance with AI” feature that nudges users to rebalance toward long-term themes. A responsible rollout could look like this:

-

Pre-launch: run backtests across multiple market regimes and publish a summarized performance report (not a promise, but empirical evidence).

-

Pilot: launch in a limited geography with a clear consent flow and opt-in beta terms that explain data use and limitations.

-

Human oversight: include a human review queue for large or unusual rebalancing requests flagged by risk heuristics.

-

Clear UI: show the user a before/after portfolio with confidence bands and “why” bullets (what signals changed, what assumptions were used).

-

Post-launch monitoring: continuously measure real user outcomes (return, drawdown, churn) and run fairness checks to detect disproportionate impacts.

-

Regulatory reporting: prepare periodic reports for the regulator summarizing incidents, model updates, and user outcomes.

This kind of staged, evidence-driven approach reduces the chance of large, systemic missteps and creates a template regulators and other fintechs can emulate.

11. The broader industry context — retail investing, AI, and financial stability

Nemo operates into a wider trend: democratized trading + automated advice. As more retail capital flows through algorithmic suggestions, systemic linkages form. If many platforms are trained on similar data and push the same themes, flows can become endogenous and amplify volatility (e.g., concentrated bets in meme or thematic stocks). That’s why exchanges and regulators pay attention to algorithmic recommendation ecosystems even if each platform’s individual models are benign.

Nemo’s decision to emphasize diversified thematic buckets, user education, and ADGM regulation helps mitigate some of these systemic risks, but broader cooperation across platforms — standards for explainability, shared anomaly-detection signals, and best practices for theme construction — would improve market health.

12. Recommendations for Nemo’s next 12 months

If I were advising Nemo (product + compliance teams), I’d suggest the following prioritized roadmap:

-

Publish model cards and performance summaries for the flagship AI features (portfolio insights, thematic discovery).

-

Open a limited independent audit (technical + fairness) and publish a summary of findings and remediation steps.

-

Introduce explicit consent toggles for model-training datasets (allow users to opt out of contributing behavioral data).

-

Build a governance council with external advisors (finance, data privacy, behavioral science) to review new AI products before launch.

-

Standardize explainability UI across the app: consistent “why,” “what if,” and confidence indicators.

-

Engage proactively with target regulators (beyond ADGM) to map suitability and disclosure expectations for each market.

-

Measure long-term investor outcomes (12–36 months) and publicly report anonymized metrics as a measure of product efficacy.

These steps are practical, defensible to regulators, and beneficial for user trust — they would make Nemo a leader rather than merely a fast follower.

13. What investors should ask before accepting AI advice from Nemo or any app

Before taking automated or AI-guided investment advice, retail investors should ask:

-

What exactly does the AI recommend and why? (Ask for plain-language summary and confidence/uncertainty information.)

-

Has this feature been backtested against stress periods? What were the results?

-

How does the app measure suitability for my profile, and can I override it?

-

What data do you collect, how long is it retained, and is it used to train models? Can I opt out?

-

Who is liable if an AI recommendation causes loss? What is the dispute resolution path?

-

Is there human oversight for major or unusual recommendations?

Good answers to these questions separate responsible providers from marketing-led ones.

14. Conclusion — pragmatic optimism, not hype

Nemo.money embodies a pragmatic path for AI in retail investing: packaged education, thematic discovery, and incremental automation under a recognized regulatory umbrella. CEO statements and recent product launches show that the company understands both user opportunity and the compliance friction that follows. That said, the real test will be execution: transparent documentation of models, measurable safeguards, and a demonstrable focus on long-term investor outcomes.

AI can lower the barrier to sensible investing and democratize access to analytics that were once the preserve of professional teams. But without rigorous design, testing, and clear regulatory alignment, AI-guided recommendations can mislead users with convincing but fragile signals. Nemo has an opportunity to set a new standard: combine accessible UX with rigorous disclosure and governance — and in doing so, prove that AI can be an asset to retail investors without sacrificing safety or integrity. EIN PresswireCryptoSlate

Sources & further reading (selected)

-

Nemo.money official site (product pages, learning hub). nemo.money

-

Nemo.money CEO Nicholas Scott interview — CryptoSlate / SlateCast (Aug 19, 2025): discussion on AI-guided investing, data veracity, and regulatory contrasts. CryptoSlate

-

Nemo.Money introduces AI Personalized Portfolio Insights (May 2025 press release summary). EIN Presswire

-

CryptoSlate feature: “How Nemo.money is redefining global investing” (product/regulatory context). CryptoSlate

JPMorgan and MUFG Near $22 Billion Data Center Financing Deal in Texas, FT Reports